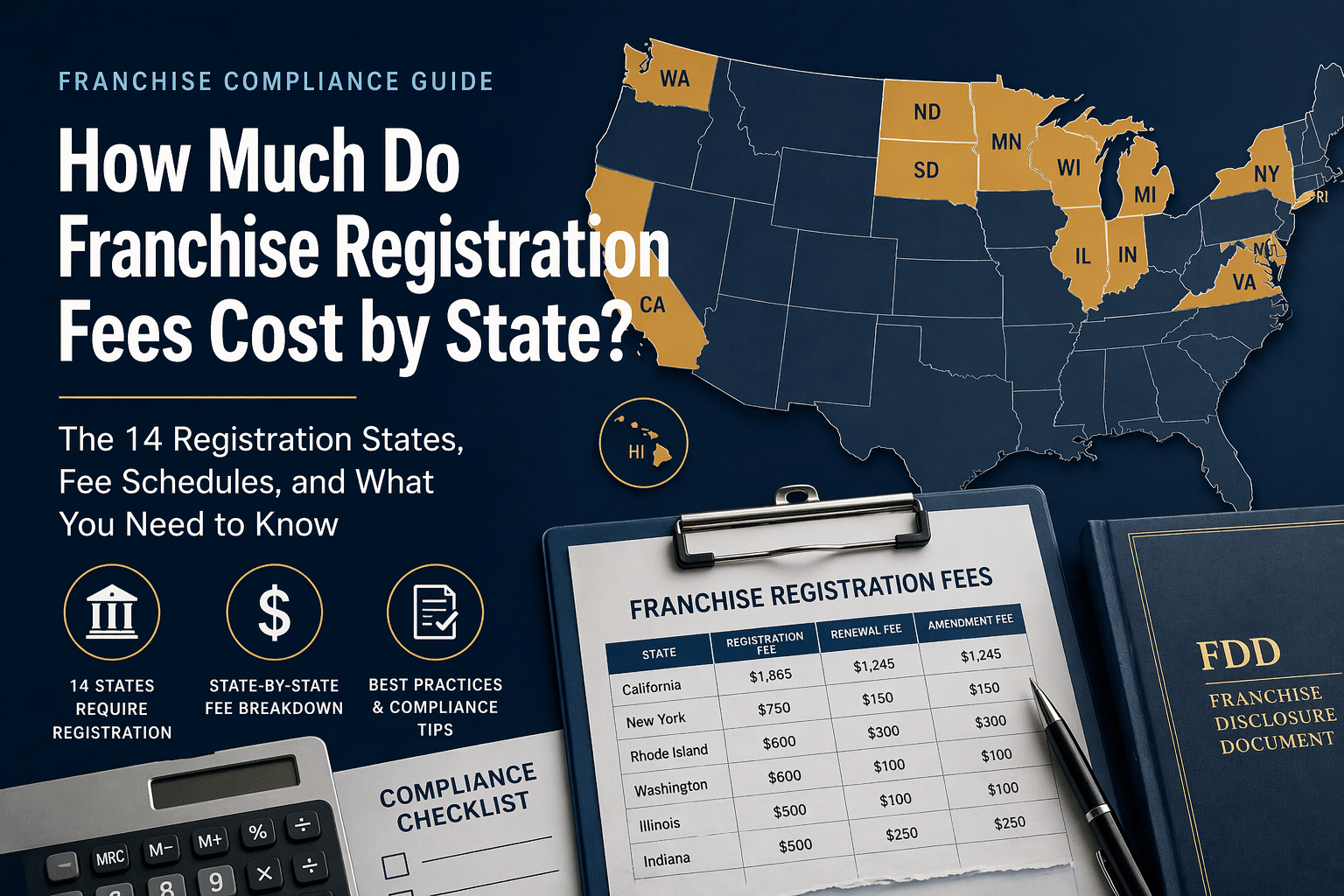

Which States Charge Franchise Registration Fees – and What Are the Best Practices for Each? April 23, 2026 No Comments Read More »

Franchise Advertising Rules: Which States Regulate Them and What You Need to Know March 26, 2026 No Comments Read More »

Protecting Your Momentum: Navigating Material Changes and FDD Updates February 21, 2026 No Comments Read More »

Franchise Law Explained: When to Provide the FDD and How to Pre-Qualify Candidates January 21, 2026 No Comments Read More »

How to Legally Offer and Sell Franchises: A State-by-State Guide January 16, 2026 No Comments Read More »

Franchise Law Explained: When to Provide the FDD and How to Pre-Qualify Candidates October 21, 2025 No Comments Read More »

Should a Non-Disclosure Agreement be signed before the FDD is provided? When and Why October 21, 2025 No Comments Read More »